")

{kind=link}

by Richard Kastelein — Publisher Blockchain News

Andrzej Horoszczak grew up under Communism in Warsaw, Poland ― and his perception of money evolved under a system that drilled the idea that everyone in a given society should receive equal shares of the benefits derived from labour.

The 80s he grew up in saw martial law, a suspended Solidarity Party with temporarily imprisoned leaders, heightened controls on civil liberties and political life, as well as food rationing. All this pretty much remained in place through the decade. They were tough times.

“Our concept of money under Communism is hard to explain,” said Horoszczak, from his trendy office in central Warsaw. “Not everything was measured by money, to be a millionaire was useless.“

Back then the West and its aura of wealth and money was a mystery to Horoszczak and one that eventually drove him to leave Poland to explore and discover himself what makes our world tick when it comes to capitalist society.

“To me it seemed that money determined all in the West.”

With the fall of Communism in Poland and the first free elections since the War (June 4th, 1989), the doors opened up in Poland and also… for Horoszczak. he crossed the pond to studying computer engineering in the USA in the early nineties, to start his MBA in Finance and Financial Management Services at The Wharton School ― the University of Pennsylvania, to satiate his desire to figure out this mysterious money world that was rather diametric to the one he grew up in under the boot of the Soviet Union.

While studying at Wharton, he picked up a job at First Fidelity Bank in the IT department to help fund his schooling and it was there he had a revelation.

“It was amazing when I realised that money was simply an ASCII string, written in COBOL, housed in an SQL database,” said Horoszczak.

He could not believe it was simply that simple. And that primitive.

“That was when I realised it could be changed ― it had to be changed.”

From Wharton, the young Polish computer engineer MBA graduate bounced around Wall Street and The City in London as an investment banker for seven years before eventually returning to Poland.

That idea that money needed to be and could be changed stuck with him, however. It always was at the back of his mind.

So in 2008, he began to merge his experiences in the financial world with his computer engineering skills and surrounded himself with a number of cryptographers and mathematicians in Warsaw in order to start exploring the idea of how money could be changed. This was around the time when Satoshi Nakamoto published his Bitcoin paper describing the Bitcoin protocol which finally solved the Byzantine Generals Problem (or Two Generals Problem) in a practical way ― figuring out the challenge of taking a safe decision while communicating with other parties over an insecure network.

Horoszczak considers Nakamoto more of a philosophical peer than a technological one.

“We both wanted to start from scratch and make money better,” added Horoszczak. “We had the same questions as Satoshi around the same time period”.

In the late 2000s and early 2010s, the algorithms really started to emerge in cryptography that truly made it possible to change the financial system.

“The math did not exist 20 years ago,” he said. “It’s a bit like when we figured out atomic fusion ― it’s like ― what do we do with it now?”

And in many ways, Poland was the perfect place to hack the math. The tradition of cryptography and cryptology runs deep through the society, which is already renowned for its mathematicians and engineers.

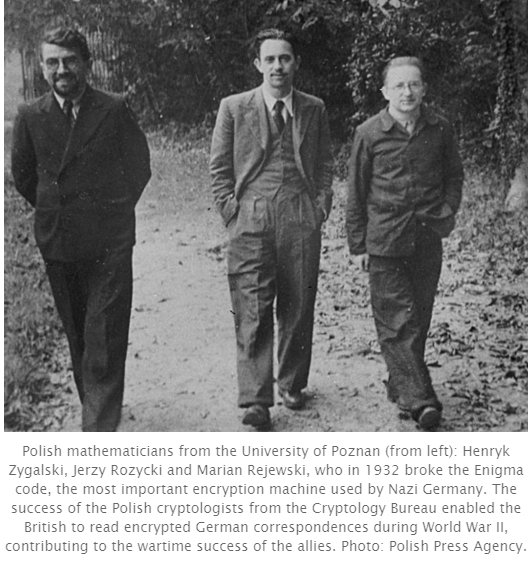

For example, the brilliant Polish cryptologist Marian Rejewski attacked and ‘broke’ the early German Army Enigma system (an electro-mechanical rotor cypher machine) using theoretical mathematics in 1932.

In cryptography circles, it was then considered the greatest breakthrough in cryptanalysis in over a thousand years since the Arab mathematician and polymath Al-Kindi (also known as Alkindus) wrote a book on cryptography in the 9th century, entitled Risalah fi Istikhraj al-Mu’amma (Manuscript for the Deciphering Cryptographic Messages), which described the first known use of frequency analysis cryptanalysis techniques.

Despite Hollywood’s glamorous portrayal in the movie The Imitation Game ― with Benedict Cumberbatch as a real-life British cryptanalyst Alan Turing, saving the West by breaking the German war machine, it was the Poles who broke it first. Poland’s fundamental work in Enigma decryption was unfortunately omitted from the movie.

Poland today is still chock full of crypto-talent with a plethora of learning facilities including the Polish Defense Ministry’s National Cryptology Center, the Cryptology and Data Security Group at the University of Warsaw, the Cryptography & Network Security department at the University of Wrocław and the Faculty of Cybernetics at the Polish Military University of Technology.

It was in this hotbed of cryptography talent that, seven years ago, Horoszczak began his idealistically-driven journey to change money and he began to seriously work with some of the finest cryptographers, mathematicians and computer engineers in Warsaw. he eventually dropped his job running a large publishing company and four years ago he launched his startup called Billon, which is the ancient word for the alloy used to create a metallic coin.

For a time, he largely financed the operation with own funds and research grants but soon began to look for outside investment. In 2014, in stepped American Angel investor David Putts, an American expatriate out of Chicago, based in Warsaw. Putts is a veteran banker and ex-McKinsey & Company. No stranger to the banking scene, he built three banks from scratch to over 200 staff ― including Poland’s first direct bank (Inteligo), HSBC’s regional CEE Premier Banking division, and Equa Bank, the most aggressive direct/mortgage bank in the Czech Republic. Putts is now an investor in good ideas.

“I turned them down twice before coming around,” said Putts with a smile. He’s now the Chairman of the company.

That’s not surprising really. Even though Putts is a forward-thinking banker, getting onboard a startup that uses technology derived from Bitcoin in 2013–2014 was pretty brave. Bitcoin was truly being dragged through the mud in those days due to its use by drug dealers, money launderers, and paedophiles, and it’s status as de facto currency of the Dark Web didn’t help.

But it was the viable potential to get it greenlit by regulators and get it backed by the banks that really gave him the confidence to invest. It was not about Bitcoin, it was the Blockchain that was key. He realised that early on.

In late 2015, this is now pretty much standard thinking in the banking world as the R3 blockchain organisation has now herded 42 of the world’s largest banks into a consortium to investigate Blockchain and Linux is now spearheading a new movement along with the likes of Deutsche Boerse, JP Morgan, Cisco and IBM to build a new blockchain-based on open source technology.

Blockchain is a potential gamechanger. And everyone seems to now be jumping on the bandwagon.

But it appears that Poland is ahead and already changing the game now ― with the world’s first blockchain-enabled, bank-backed transactions that are compliant with regulators which allow for bankless banking. Billon.

“This is important ― mass adoption can only occur if clients are using their existing mobile phones and favorite local currency,” said Horoszczak. “Today, payments are a broken end-to-end value chain full of intermediaries, payment insurers, liquidity providers, clearing agents, settlement agents, and account holders. Imagine giving the power to truly provide an end-to-end solution…and eliminate all the cost, risk, and hassle that exists today.”

Simply put, Billon is a peer-to-peer payment system based on the Blockchain solution more commonly associated with Bitcoin. In contrast to widely Bitcoin it is not a currency and therefore technically it is a not cryptocurrency, but rather it is considered crypto-cash. And the uniqueness of this system lies in the fact that while it brings the huge cost advantage of infrastructure based on a distributed blockchain, it is fully legal and based on a national currency ― currently the Polish Zloty.

So how is it different from Paypal? Paypal is integrally connected to the traditional banking system. There are 13 steps needed for validation. Billon needs two as it operates independently of the banking system. Getting money out of Paypal takes days, rather than immediately with Billon. Paypal has internal fixed costs of about ten cents per transaction which means it’s not financially viable to use Paypal for microtransactions. The Blockchain solves this cost issue as the user bears a variable cost as part of the Blockchain itself.

“Transactions using legacy systems are unprofitable below 10 euros, and with Billon, every transaction is profitable,” said Horoszczak.

He then went on to show a demo of Billon being used to pay ten cents for a single article online, adding that it’s feasible when using Blockchain technology to do micropayments of this sort.

Billon is now working with Twitch streamers in Poland. There are three million Twitch users in the country and it is the glue connecting Twitch streamers and other content creators with an audience that can now simply and easily tip them using a seamless system of micropayments.

To collect tips, Twitch broadcasters and content creators simply add a button to their streams for their audience to click. Fans can top up their accounts using various methods such a small shops (they have a deal with 28,000 stores in Poland for top-ups), bank transfer, or credit card and reward their heroes. The system allows receivers (content creators in this case) to cash out in a number of ways including cash directly from an ATM using a code (cardless) or bank transfer to their own accounts. In Poland, you can take money out of an ATM without a card by using only a code ― which Billon helped lobby the government and bank officials to introduce in the country.

Twitch primarily focuses on video gaming, including playthroughs of video games, broadcasts of e-sports competitions, and more recently, creative content. Content on the site can either be viewed live or viewed via video on demand. In 2015, Twitch announced it had more than 1.5 million broadcasters and 100 million global visitors per month.

Billon’s first substantial deal is with Handi.cash, an EU based player with multiple country aspirations, but with a strategy still undisclosed. Additionally, they are working on more deals in Poland and plans to expand outside the country are in action.

“We are working with a large European bank which can’t yet be named,” said Chairman Putts. “Our plan is to move into the Euro and Pound and continue to expand internationally from there.”

The Billon blockchain system is currently backed by two large Polish financial institutions ― Alior Bank and PlusBank ― and adheres to both Polish and EU regulations.

Unlike Bitcoin, there are no miners in Billon. Instead, the Genesis blocks in Billon’s blockchain, are created by an authorised issuer ― in this case, two licensed Polish banks.

All the users need is software that contains the public keys of the issuers, and just like a bitcoin wallet, has to be capable of parsing Billon’s digital Blockchain format and verifying signatures on incoming and outgoing money.

Both the sending and receiving party have to register their public keys at the issuing bank and this is done automatically during the registration process. To set it up, users of the system choose a login name and generate their own private keys which are presented to the bank for authentication. Once the one-time registration process is completed, the software automates all the cryptography and the user is only required to click “Yes” or “No” to confirm payment.

In contrast to Bitcoin’s Blockchain, the speed of transaction is orders of magnitude faster and for a typical transaction, it’s less than 10 seconds.

“Our design goal was to provide the same speed of transactions as contactless payment cards with much lower fraud levels, working not only in the physical shops but also between the computers over the Internet and directly between smartphones,” noted Horoszczak. “We are getting closer and closer to ‘beep… I paid’. “

“With Billon there’s not need to compress history into a hash and keep terabytes of data,” he added. “This is what gives us the speed that Bitcoin just can’t.”

As opposed to Bitcoin which has created a slew of mining factories around the world which take up huge resources in terms of energy, Billon is a much more sustainable and eco-friendly option. The energy footprint of Bitcoin is appalling. According to one calculation, a single Bitcoin transaction uses roughly enough electricity to power 1.57 American households for a day. Bitcoin is about 5,033 times more energy-intensive, per transaction, than VISA and according to Forbes, and Bitcoin mining uses $15 million dollars worth of electricity every day.

Billon does not have this problem. Once Billon crypto-cash is converted back to fiat currency (electronic or paper cash) the blockchain is destroyed (like old paper money is destroyed).

Billon is created by and inside the issuing bank ― which essentially digitizes a pooled account of currency into Billon’s Blockchain digital cash. The digital cash is a kind of standardized file with a Billon specified crypto-protocol standard which allows interoperability between multiple blockchains representing digital cash issued by multiple banks.

Once the Billon blockchain is created and transferred by the bank to the first user, further circulation is done entirely on a peer-to-peer basis without any further involvement from the issuing bank.

The Billon denomination ranges from standard notes 200, 100, 50, etc. down to a very low 1/10 of one grosz (Polish cent).

And this is where things start to get even more interesting.

These tiny amounts are called nano payments and can be used to reward or pay people tiny amounts of real money for doing small actions. It also opens up possibilities for direct machine-to-machine price settlements a future where Blockchain meets the Internet of Things. And economically feasible micropayments can absolutely change the publishing world, for print media and music in particular.

Conceivably, Billon also makes it possible for some 2.5 billion adults across the globe without bank accounts to enter the digital economy.

Merchants or users that want to convert digital cashback to electronic or paper cash can simply transfer the money out to their bank account or take the money out of an ATM machine with a code issued from the issuing bank to their Billonsmartphone application (cardless withdrawals are permitted in Poland).

As a Billon user, one does not need any bank account nor any other banking product (cards, cheques, etc.) and anyone with a computer or smartphone can start using digital cash from the get-go.

Seeing the technology infrastructure and architecture is Blockchain-based, and is not core-banking system-based means that data that is transmitted between Billon applications is encrypted, and never stored on any server. Therefore even if someone breaks into a financial institution that issues your digital cash, the hacker cannot steal your money, cannot steal information about your transactions, and cannot force you to change passwords ― simply because this information is not stored in the bank, so there is nothing to be stolen.

Blockchain solves the key technological problem of banks ― how to protect access to confidential data. With Billon, all data is stored on users’ devices, and all transactions happen on a peer-to-peer basis, meaning when users move money between one another, bank central infrastructure is never used. This means radical cost savings for the banks. No more transaction processing costs, no more transaction authorizations, no more transaction settlements, no more transactional counterparty risk, no more transactional chargeback procedures, no more IT infrastructure designed to handle transactional peak volumes.

The bottom line is that it simply saves banks tons of money and also allows them to onboard potentially new clients who currently don’t have bank accounts. And it saves banking customers and merchants a lot of money in transaction fees.

Billon also complies with Polish and EU banking requirements in regards to Know-Your-Customer (KYC) and Anti-Money-Laundering (AML) and banking regulations (both internal and legal).

The product was created by a team of over 30 IT specialists, including cryptologist, network and cloud engineers and system integrators. All of the team members graduated from top engineering schools, with the majority having lengthy experience with blue-chip companies like HP, Samsung, IBM, Naspers, Cisco. Billon is proprietary, but offers open APIs and can be white labelled.

But critics of private blockchains like Billon say that it’s simply the same old story, however… with banks being at the helm, nothing changes and allowing the banks to continue as trust agents are simply not going to work. Private Blockchains to some hardcore Bitcoin enthusiasts are considered not to be true Blockchains but rather because they don’t utilise Nakamoto’s consensus architecture with miners, are merely distributed ledgers with no game-changing innovation.

Will Billon disrupt the system eventually? Who knows, but they are certainly blazing a trail by being first through the gates. Both Putts and Horoszczak expressed they felt the system needs to change but by working with the stakeholders of the trust mechanisms currently in place ― the banks ― and not against them. And by working closely with the regulators.

In other words ― a kind of slow paradigm shift to a future where our current trust merchants ― the banks ― are thinned out and are made more accountable, more transparent, and more efficient.

See the Billon promotional video below.